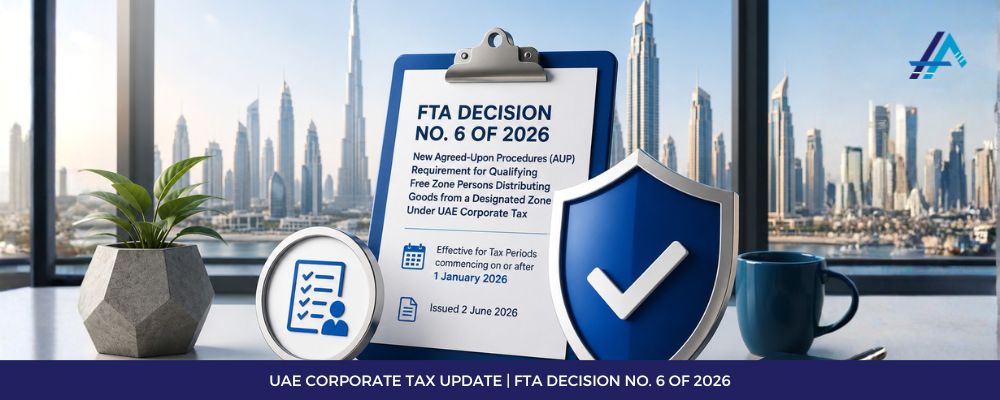

Qualifying Free Zone Persons Distributing Goods from a Designated Zone

FTA Decision No. 6 of 2026 requires QFZPs distributing goods from a Designated Zone to obtain an ISRS 4400 AUP report. Deadlines & requirements inside.

UAE Cabinet Decision No. 129 of 2025. Key Changes and Business Implications

Comparison of Administrative Penalties: Cabinet Decision 108 of 2021 vs. 129 of 2025

Stay Ahead of UAE Tax Reform: The Essential Guide to Transfer Pricing with HAS Global Tax Consultants

Stay Ahead of UAE Tax Reform: The Essential Guide to Transfer Pricing with HAS Global Tax Consultants